Biomass Heating Comes of Age: Not Just Woodchips & Cordwood Anymore

Guest Blog By Jim Van Valkenburgh, VP Sales & Marketing at Froling Energy in Peterborough, NH

The use of Biomass as a heating fuel has a long history in New England but it seems to be under-appreciated by the general public. Solar arrays that are popping up all over our region are getting a lot of attention lately but Biomass is still providing more kilowatts of energy than all of the Solar system combined. Those are kilowatts of both heat and electricity derived from wood in power plants, boiler systems, plus wood and pellet stoves in countless homes.

The people of Froling Energy are happy to be a part of the modern wood heat movement that has so positively impacted the economies of broad rural areas of New England. Having a new paying market for low grade wood is very important to loggers due to the shutting down of numerous paper mills and wood fired power plants. We believe that much more can be done with Biomass for heating all kinds of buildings and this will have real, positive economic impacts on our region.

Froling Energy has focused on the technology of biomass boilers for almost 10 years and has accumulated a long list of happy customers who, all together, are no longer burning over 1 million gallons of fuel oil each year.

As with most businesses, technology and innovation have made significant improvements in the biomass industry. It may surprise many that most of this development has happened in Austria. Twenty years ago the Austrian government made a commitment to convert a large percentage of their energy use to biomass. Today, modern biomass heating systems are commonplace in large and small buildings and Austrian boilers are the most advanced in the world: clean burning, fully automated and very reliable. As a result, they dominate the US biomass market.

Observing what is happening in Austria now allows one to gaze about 10 years into the future of the US biomass market. What can we see there? Today their biomass market is divided up fairly evenly among 3 distinct biomass fuels: Green Chips, Dry Chips and Pellets.

- GREEN (not dry) WOOD CHIPS began the movement of the automated central heating of buildings using biomass.

- PDCs—Precision Dry Wood Chips have come along to fill the wide gap in cost and adaptability between Green Chips and Pellets.

- WOOD PELLETS were an important new fuel starting about 2005: a versatile, simple to use fuel that is easy to transport and deliver.

You may be asking, “What about woodstoves?” Our industry is focused on fully automatic, self feeding central boiler systems. Any devices that are manually loaded, like a wood stove, chunk wood boiler or pellet stove, are not considered in this discussion.

The US central biomass heating market is split between Green Chips and Wood Pellets. Dry Chips account for less than 1% here. (Froling Energy is looking to change that—read on.) Let’s look at the two extremes of the market that have taken hold in the US: Boilers that burn Wood Pellets and very large boilers burning Green Chips.

GREEN WOOD CHIP BOILER SYSTEMS

Green Chip systems make the most financial sense for organizations that are BIG fuel users. There are many successful installations of large green chip boiler systems on rural campuses and public schools in Vermont, New Hampshire, Massachusetts and New York. Green chip boiler systems tend to be most common in situations where they are offsetting 100,000 gallons of fuel oil or more per year.

While a fresh cut log would be nearly impossible to light in a wood stove or fireplace, fresh wood chips burn well in a green chip boiler. That is because the chips go from wet to dry fairly quickly as they enter and pass through the boiler. By the time they make it to the fire grate, the heat of the boiler has driven out the moisture so that they burn very well.

Green wood chip boiler systems have evolved nicely to be quite well automated and reliable, but they are only economically viable for heating campuses and other large multiple building complexes. This is due to the large infrastructure costs required to purchase and install the large scale material handling and boiler systems. Big green chip boilers are typically fired up around Thanksgiving and run straight through until about the first day of Spring. They modulate their output, adjusting to a heat load like a pellet boiler, but they don’t turn off and cannot turn low enough for the intermittent loads of fall and spring.

A ton of Green chips is significantly less costly than a ton of Pellets to buy (75% less+), however nearly twice as many tons are required to generate the same amount of heat. That’s because green chips contain between 40% and 55% water by weight. Part of the heat from the burning chips is used up when that water is boiled off inside the boiler.

Burning Green Chips brings with it a number of other costly requirements: Large volumes of Green chips need to be stored under cover, usually in large boiler buildings with deep concrete pits and “live floor” material handling systems operated by complex hydraulics and connected to big augers and belt conveyors that move the chips into the boiler. These buildings must have large garage doors that 18 wheel trucks frequently dump their loads into. Particulate matter in flue gas is a concern for all biomass boilers and green chip boilers tend to need expensive Electrostatic Percipitators and/or other expensive devices in order to pass local clean air regulations.

Green chips need to be purchased from reliable suppliers—not just low bidders. This cheaper, rougher, and more basic fuel simply requires more monitoring by a trained staff. Green chips must be managed well by technicians to prevent mold growth and freeze-ups.

Maintenance staff must also keep their eyes on the big, complex green chip mechanical systems.

WOOD PELLET FIRED BOILER SYSTEMS

The earliest “fully automatic” pellet boilers from Europe were first imported to the US in 1997. Initially it seemed that these boilers were ready for commercial use and many were installed. Unfortunately they required too much manpower to keep them running reliably. They could run for a few days without attention but once a week cleanings were mandatory and daily check ups proved to be good practice. “Burn-backs” occasionally happened where the fire in the firebox would migrate through augers into the pellet feed system, creating a dangerous situation. Improvements were needed.

Around 2010 (when Froling Energy got into the business) a new generation of fully automated pellet boilers began to be imported from Austria by OkoFEN and Froeling. The systems proved to be much more reliable so sales grew steadily with the help of a couple of solid US distributors. With boilers ranging from 40,000 to 200,000 BTU/hour, a wide range of residences and small commercial buildings like town halls, churches and small schools installed systems. Staging 2 or more of them together was an effective way to get more firepower.

Sales were good and as time passed Froling Energy got into progressively larger installations. We went from installing fairly small boilers in homes and small offices to multiple boilers that could heat large areas. In the past few years we are installing biomass boilers with outputs of one to three million BTUs as a matter of course. New England Wood Pellet in Jaffrey had established itself as a reliable supplier of bulk wood pellets at a steady price. Times were good. The price of oil was averaging $3 a gallon and people were looking for options to oil. Wood pellet boilers had become a least cost, viable alternative.

Why did people buy pellet boilers? We found that fuel cost savings drove most of these purchases. Anyone with green leanings will be happy that a viable biomass option was available but if the savings of a fuel switch didn’t pay for themselves in less than 10 years it was unlikely that a project would go forward.

We discovered that larger pellet boiler systems typically pencil out better than small ones. If more fuel is being offset you get more savings. And if you add in an old, failing oil boiler and/or a leaking 10,000 gallon oil tank, an investment in a biomass boiler system has a better return on investment than any conventional options. Within a few years we were installing one and two million BTU/hour pellet boiler systems in schools and commercial businesses.

Things were going well in the biomass boiler business for Froling Energy. Customer systems were not without problems but we pushed through, learning all the way, building a solid customer base. Froling Energy has focused on customer satisfaction since day one—fixing troublesome boilers and always working to make things right.

A NEW FUEL IN THE US: PDCs—SEMI-DRY WOOD CHIPS

Back in Austria and in much of northern Europe where the biomass heating market is mature a third fuel has evolved. Pellets are a perfect refined fuel for small boilers and green chips are the least cost fuel for big fuel users–but at a time today of $2 per gallon oil, neither of these systems pencils out very well in terms of Return on Investment. PDCs have changed that, especially in the medium to large boiler market. PDCs (precision dry wood chips) are green wood chips that are chipped down to a smaller size and then dried down to 25% moisture content. They are made under quality control standards that result in a more consistent product—similar to wood pellets.

PDCs are 35% less costly than wood pellets and can be delivered by a blower truck through a 5” diameter pipe. That’s a significant difference. The usual way of delivering any kind of wood chips is by a live floor truck. Being able to blow them into a silo cuts the infrastructure costs by $150,000. Not having to construct a building containing storage pits with live floor material handling systems saves at least that much money again. Not having to maintain all that extra equipment saves a lot in man hours over the years.

PDC boiler systems are a hybrid that costs about 10% more than a similar pellet only system. The biggest differences from a pellet system are the size of the silos and the mechanics of the material handling system that brings fuel from the storage silo to the boiler. Pellets flow like water while PDCs (and Green Chips) stack up. If pellets are drawn out from the bottom, pellets from above flow downwards. If chips are pulled from the bottom, the upper chips just stay in place. Force must be applied to make them move. The most common and least cost method is a rotary extraction device or “sweeper arm” which moves under the pile, pushing chips into an auger channel below everything. From there, rigid augers move the PDCs directly into the boiler.

Most European pellet boilers over 500,000 BTU/hr can burn either pellets or PDCs. If a system is built to handle PDCs, it can also burn wood pellets as a “back up fuel”. However a system that’s built for pellets is not able to move PDCs.

Who manufactures PDCs? Froling Energy makes and delivers them in blower trucks to multiple customer sites. One other company in New Hampshire makes a semi-dry wood chip and delivers them in live floor trucks. We expect others to join into this market as it expands.

FUEL COMPARISONS

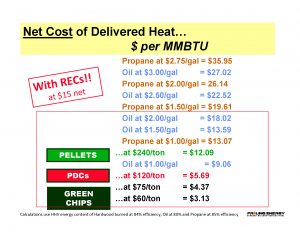

Price per ton of each of these three important biomass fuels is surprisingly different. But don’t be fooled by price per ton because increased cost is due to increased value to the customer, which is added by levels of processing. To replace 10,000 gallons of fuel oil you would need 83 tons of pellets, 107 tons of PDCs or 162 tons of green chips. All three are sourced from the same wood material. Water content and size/shape are the biggest variables which impact the ease of handling, delivery methods, and stability on site.

THERMAL RECS

What are Thermal RECs? Renewable Energy Certificates. RECs are bought by power companies who are required by each state’s Renewable Portfolio Standards to generate fixed percentages of their delivered power from renewable sources. Solar RECs are quite commonly understood as one of the key factors to making practical the generation of electricity with solar photovoltaic arrays. Where solar systems create RECs by generating megawatts of electricity, biomass boilers create Thermal RECs based on the net amount of heat they produce.

New Hampshire was the first state to authorize Thermal RECs. Today, NH Thermal RECs can be sold for between $12 and $25 each. Thermal RECs are only available in New Hampshire at this time but Massachusetts is making plans to offer them in 2018.

Burning one ton of pellets can generate about 4 T-RECs while a ton of PDCs generates about 3 and Green Chips generate about 2 per ton. (These are rounded estimates. Each situation will vary.)

PDCS REVITALIZE A DIFFICULT MARKET

In recent years where the price of oil has pushed below $2 a gallon, the availability of PDCs with a net cost of about 80 cents a gallon of oil have kept our crews busy. Wood pellet systems have lost momentum. As a result, most of the new boiler systems that we have installed lately have been set up to burn PDCs.

PDCs make a biomass boiler system a much better investment and have the potential to add growth and stability to the low grade wood market in New England. Our most recent PDC Boiler projects include the Merrimack County Jail in Boscawen, NH, Plymouth Regional High School in Plymouth, NH, a third PDC boiler room at Whelen Engineering in Charlestown, NH and the Applegate Housing Project in Bennington, VT. This summer our crews remain very busy doing boiler installations. We see a bright future in this industry so long as we keep advancing the technology.

Download a PDF of Froling Project – Merrimack County Department of Corrections here: http://bit.ly/2sJLH8q

Download a PDF of Froling Project –Whelen Engineering Boiler System #3 Burning PDCs: http://bit.ly/2rUNkNF

590 Hancock Rd

Peterborough, NH 03458

603-924-1001

FrolingEnergy.com

Jim@FrolingEnergy.com